GROUNDED DEFENCE

As PLife REIT embarks on its next phase of growth,

we remain rooted in preserving the valued resiliency

which we have conscientiously seeded over

the years.

To maintain a robust financial position and strong

balance sheet, we have pre-emptively termed out all

our debt facilities maturing in FY2015 and extended

the underlying long term interest rate hedge

correspondingly. As at 31 December 2014, PLife

REIT continues to enjoy a low average all-in cost of

debt of 1.4% with a lengthened weighted average

debt maturity of 3.7 years. With a well spread out

debt maturity profile and minimal refinancing risk

in the near term, the position of our balance sheet

is enhanced.

During the year, PLife REIT’s natural hedge strategy

and its prudent 100% net income hedge for its

Japanese currency exposure, which were put in

place since its first acquisition in Japan in 2008,

continues to provide effective shields against

volatility of the Japanese Yen. Despite the continual

depreciation of the Japanese Yen in FY2014, PLife

REIT was insulated against this drastic currency

move and managed to grow its DPU by 7.1% in

spite of the challenge. This strategy has also helped

PLife REIT maintained a stable net asset value at

the same time.

As a testament to PLife REIT’s solid fundamentals

and sound financial metrics, in 2014 Fitch affirmed

PLife REIT’s long-term issuer default, senior

unsecured rating and the S$500millionmulticurrency

MTN Programme (the “MTN Programme”) at ‘BBB’,

with a stable outlook. Additionally, PLife REIT was

for the first time assigned by Moody’s Investors

Service (“Moody’s”), a ‘Baa2’

[3]

issuer rating in 2014

as well as a provisional ‘(P)Baa2’

[4]

senior unsecured

rating to the MTN Programme, with a stable outlook.

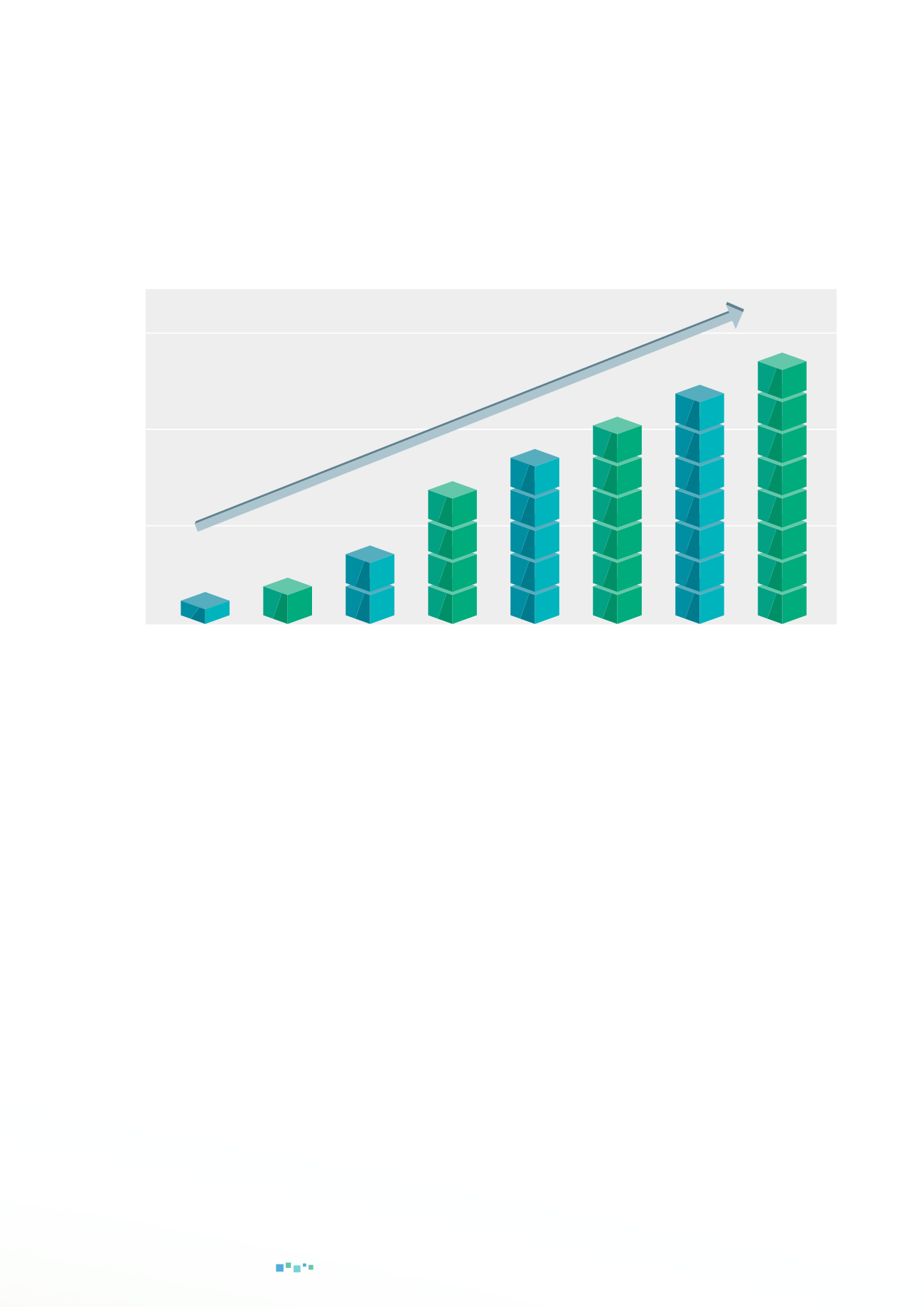

DPU

(cents)

12.0

10.0

8.0

6.0

FY 2007

(annualised)

FY 2008

FY 2014

FY 2013

FY 2012

FY 2011

FY 2010

FY 2009

11.52

10.75

10.31

[2]

9.60

8.79

7.74

6.83

6.32

STRONG DPU GROWTH SINCE IPO

DPU has grown steadily at a rate of 82.3% since IPO

[1]

+82.3%

[1]

YTD 4Q 2014 accumulated DPU payout since IPO is 67.81 cents (inclusive of 3Q 2007 pro-rated payout)

[2]

Since FY 2012, S$3.0 million per annum of amount available for distribution has been retained for capital expenditure

[3]

Equivalent to Fitch's ratings of BBB

[4]

Moody's only assigns a provisional rating to MTN Programme and will issue a definitive rating upon specific notes issuance

7

A N N U A L R E P O R T 2 0 1 4